Home Insurance

UAE Winter Leaks 2026: Why Water Damage Claims Get Rejected

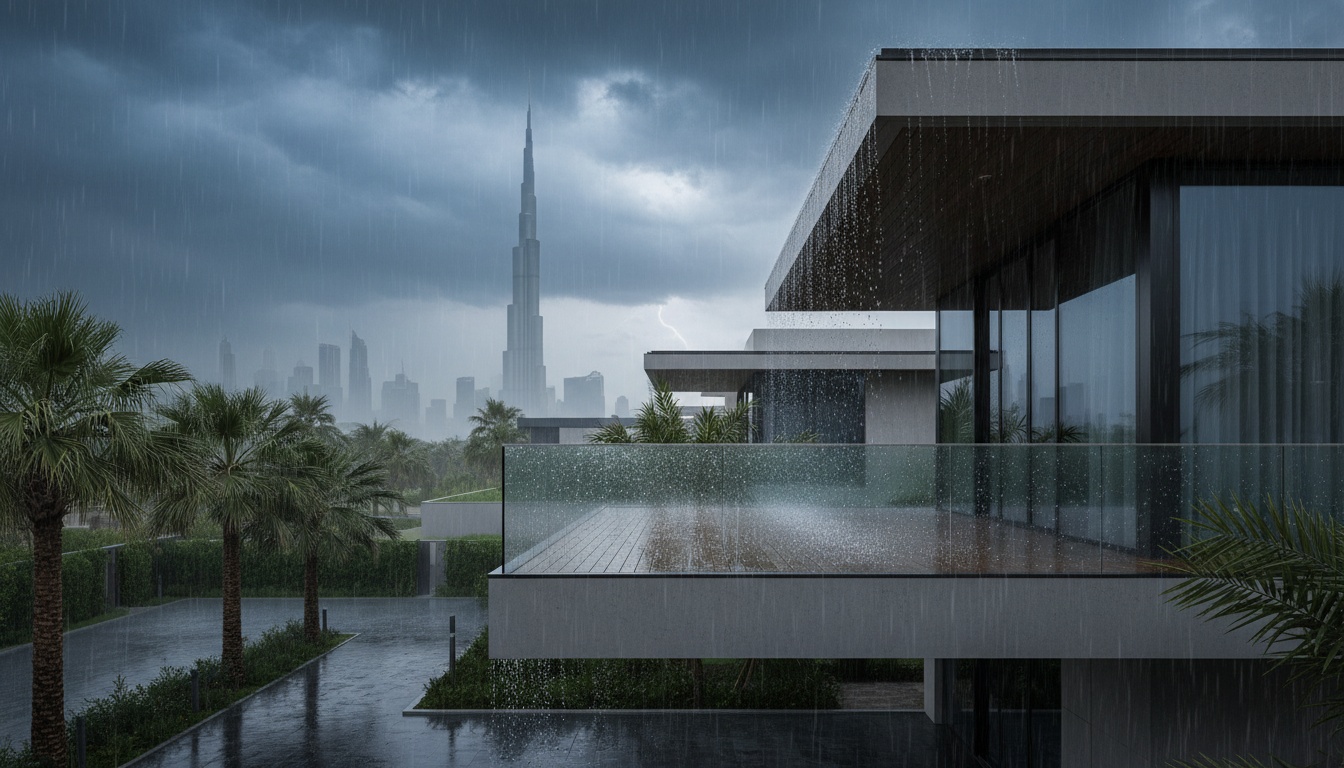

As the cooler months settle over the UAE, residents across Dubai, Abu Dhabi, and Sharjah face an unexpected challenge: water damage from winter rains and condensation. While rare, intense winter storms can expose vulnerabilities in both villas and high-rise apartments, leading to thousands of dirhams in damage. However, many UAE homeowners and tenants discover their insurance claims are rejected—often due to misunderstandings about what their policy actually covers. This article explains the critical distinctions between covered and excluded water damage scenarios, helping readers navigate the claim process successfully in 2026.

Understanding Water Damage Coverage: Sudden vs. Gradual Ingress in the UAE

Home insurance policies in the UAE make crucial distinctions between different types of water damage. The fundamental divide lies between "sudden and accidental" events versus "gradual" deterioration—a difference that determines whether insurers honor claims.

Escape of Water refers to internal plumbing failures: burst pipes, overflowing water tanks, or malfunctioning appliances. When these occur suddenly, most comprehensive home insurance policies in the UAE provide coverage for the resulting damage to contents and, in building insurance policies, structural repairs.

Water Ingress, by contrast, involves external water entering through roofs, windows, balconies, or walls. This category becomes complicated during the winter months when distinguishing between storm-driven rain (potentially covered) and seepage from poor maintenance (typically excluded) requires careful documentation.

The 2024 UAE floods created precedents that influenced 2026 policy wording. Insurers now explicitly distinguish between "natural disaster" flooding (covered under specific endorsements) and "penetrating damp" from building defects (excluded). Tenants should verify whether their contents insurance covers water damage from building failures, as landlords' building insurance may not extend to tenants' belongings.

Key coverage elements to verify in 2026 policies:

- Limits for "Escape of Water" claims (often capped separately)

- Exclusions for "Wear and Tear" and "Lack of Maintenance"

- Coverage for consequential damage (mold, electrical damage)

- Requirements for "Mitigation of Loss" actions

- Excess/deductible amounts specific to water claims

Top 5 Reasons UAE Insurers Reject Winter Leak Claims in 2026

Understanding common rejection reasons helps residents avoid preventable claim denials. Based on 2026 UAE Central Bank complaint data and insurer disclosure requirements, these five factors account for most water damage rejections:

1. Gradual Seepage and Maintenance Failures

The leading cause of rejection. When surveyors determine water entered gradually due to deteriorated sealant, cracked grout, or aging waterproofing, insurers classify this as preventative maintenance—the property owner's responsibility. Evidence such as staining patterns, material degradation, or previous minor leaks supports rejection decisions.

2. Pre-Existing Damage

If insurance was purchased recently, insurers investigate whether damage existed before policy inception. Property inspection reports, move-in condition photos, and maintenance records become critical evidence. Many UAE policies include 30-day waiting periods specifically for water damage claims.

3. Failure to Mitigate Loss

UAE insurance law requires policyholders to take reasonable steps to prevent damage escalation. Residents who notice leaks but delay emergency repairs, fail to shut off water supplies, or don't protect belongings from ongoing water exposure may face partial or complete claim denials. Documentation of mitigation efforts—plumber receipts, emergency service calls, photos of protective measures—proves compliance.

4. Insufficient Documentation

Successful claims require comprehensive evidence. Missing elements include:

- Immediate damage photos (timestamped)

- Dubai Police or local police "To Whom It May Concern" certificates confirming weather events

- Professional assessment reports from UAE-licensed plumbers or building surveyors identifying the water source

- Receipts for emergency repairs

- Inventory lists with replacement values for damaged contents

5. Policy Misunderstanding: Building vs. Contents

Tenants frequently assume comprehensive coverage when holding only contents insurance. Structural repairs—ceiling replacement, wall remediation, flooring restoration—fall under building insurance carried by landlords. Conversely, villa owners sometimes discover their building insurance doesn't cover interior contents like furniture, electronics, or personal belongings damaged by leaks.

Get Free Quotes →

Covered vs. Excluded Water Damage Scenarios in the UAE

| Damage Scenario | Likely Status | Common Reason for Decision |

|---|---|---|

| AC pipe burst due to pressure | Covered | Sudden and accidental occurrence |

| Roof leak from missing sealant | Rejected | Lack of preventative maintenance |

| Water tank overflow from faulty valve | Covered | Mechanical failure constitutes sudden event |

| Rain flooding via balcony doors | Case-by-Case | Depends on 'sudden storm' evidence vs. 'open door' negligence |

| Bathroom pipe corrosion leak | Rejected | Gradual deterioration from wear and tear |

| Storm-driven rain through window seals | Case-by-Case | Requires proof of exceptional weather beyond normal conditions |

| Washing machine hose rupture | Covered | Sudden appliance failure with immediate water release |

This table reflects common UAE insurer interpretations in 2026, though individual policy wording and specific circumstances influence final decisions. The "Case-by-Case" scenarios depend heavily on supporting documentation, particularly weather reports from the National Center of Meteorology and police certificates confirming storm conditions.

The Role of SANADAK and the Central Bank in Dispute Resolution

When insurers reject water damage claims residents believe valid, the UAE offers formal dispute resolution mechanisms strengthened throughout 2025 and 2026.

SANADAK, the UAE's unified insurance complaint platform administered by the UAE Central Bank, serves as the primary channel for insurance disputes. The platform replaced separate emirate-level processes, creating standardized complaint handling across Dubai, Abu Dhabi, Sharjah, and other emirates.

The SANADAK process:

- File complaint online at sanadak.gov.ae within specified timeframes (typically within 6 months of claim rejection)

- Upload supporting documentation: policy documents, rejection letters, damage evidence, expert reports

- Receive case number and insurer response deadline (usually 15 business days)

- Review insurer's formal explanation and counter-evidence

- Accept proposed resolution or escalate to formal mediation

- If unresolved, proceed to Insurance Disputes Settlement Committee

The UAE Central Bank's 2026 regulations require insurers to provide detailed, written rejection explanations referencing specific policy clauses and submitted evidence. Vague rejections violate regulatory standards, strengthening policyholders' positions in SANADAK proceedings.

Success factors for SANADAK complaints:

- Professional root cause reports from UAE-licensed professionals (plumbers holding municipality approvals, certified building surveyors)

- Contemporaneous evidence (photos taken immediately upon discovering damage, not weeks later)

- Clear timeline documentation showing prompt notification and mitigation efforts

- Weather data from official sources corroborating claims of exceptional conditions

For building-related disputes involving landlord responsibilities, residents may also contact the Dubai Land Department or equivalent emirate authorities overseeing tenancy regulations.

Compare Plans →

Winter-Proofing Your Documentation: A Claim Preparation Guide

Proactive documentation practices significantly improve claim approval rates. UAE residents should implement these steps during winter months when water damage risks increase:

Immediate Response Protocol:

- Stop the water source if possible (shut valves, contain appliance leaks)

- Photograph everything immediately with timestamped images

- Contact insurer within required notification timeframe

- Protect belongings by moving items away from water, covering with plastic

- Arrange emergency repairs only after documenting original conditions

Essential Documentation Checklist:

- Pre-winter property condition photos establishing baseline

- Maintenance records proving routine servicing (AC systems, plumbing inspections)

- Weather reports from National Center of Meteorology for claim dates

- Police certificates for storm-related events

- Professional assessments identifying water source and ingress point

- Itemized loss inventory with purchase receipts or valuations

- All communication with insurers (emails, claim forms, adjuster notes)

Preventative Measures to Avoid Rejections:

- Schedule annual property inspections documenting good maintenance

- Address minor leaks immediately with documented repairs

- Maintain comprehensive property insurance covering both building and contents based on ownership status

- Review policy exclusions and coverage limits before incidents occur

- Consider additional endorsements for flood coverage if properties face elevation risks

Understanding the distinction between landlord and tenant responsibilities prevents coverage gaps. Tenants should verify landlords maintain active building insurance while securing their own contents coverage. Villa owners need comprehensive policies addressing both structural and contents protection.

Conclusion

Bottom line: Water damage claims in the UAE succeed when residents understand the critical difference between sudden, accidental events and gradual maintenance failures. The 2026 regulatory environment, strengthened by SANADAK and Central Bank oversight, provides robust dispute resolution—but only when policyholders submit properly documented claims distinguishing storm-driven ingress from preventable deterioration. By implementing proactive documentation practices and understanding policy boundaries, residents protect themselves against both water damage and claim rejections.

FAQ

Does my UAE home insurance cover mold caused by a winter leak?

Coverage depends on the mold's cause. If mold results from a covered peril like sudden pipe bursts, remediation typically receives coverage. However, mold from gradual seepage, poor ventilation, or maintenance neglect falls under standard exclusions. Policies usually require mold treatment within specific timeframes after covered water events.

How long do I have to report a water leak claim in Dubai or Abu Dhabi?

Most UAE policies require notification within 48-72 hours of discovering damage. Some insurers allow up to 7 days, but delayed reporting significantly weakens claims. Immediate notification, even before assessing full damage extent, protects claim validity. Check specific policy wording for exact timeframes.

Can a landlord claim against a tenant's insurance for water damage?

Yes, if tenant negligence caused damage. Examples include leaving taps running, failing to report leaks promptly, or damaging plumbing through misuse. Landlords must prove tenant liability. Standard tenant contents insurance includes liability coverage for such scenarios, protecting tenants from direct payment demands.

What is the 'SANADAK' process if my water damage claim is unfairly rejected?

SANADAK (sanadak.gov.ae) is the UAE Central Bank's unified insurance complaint platform. File complaints online within 6 months of rejection, submitting all documentation. Insurers must respond within 15 business days. Unresolved cases escalate to formal mediation and potentially the Insurance Disputes Settlement Committee, which issues binding decisions.

Does 'natural disaster' coverage include heavy rain in the UAE?

Standard policies rarely classify typical UAE rain as natural disasters. However, events meeting specific intensity thresholds—similar to the 2024 floods—may qualify under specialized endorsements. Most policies exclude flood damage unless explicitly purchased as additional coverage. Review policy definitions and consider flood endorsements for at-risk properties.

Will my claim be rejected if the leak started while I was traveling outside the UAE?

Potentially. Many policies exclude damage from unattended properties during extended absences. Some insurers require property checks every 72 hours when residences are vacant. Review policy terms regarding unoccupancy, arrange for property monitoring during travel, and notify insurers of extended absences to maintain coverage validity.

Editorial note: This article is for general information and does not constitute insurance advice. Always confirm terms with your insurer.